Notice: This post is a sequel…Please read Chapter I if you haven’t…

A. WHAT IS E-MONEY? A BRIEF DEFINITION

E-Money features the following properties:

- It’s a Claim to an issuer, created with value not less than the funds received in exchange for the issuance.

- It’s stored in an electronic medium.

- It’s a means of payment for undertakings other than the issuer.

Electronic Money is in fact a genuine Payment System, comprising an issuer, purseholders/consumers, and a network of Merchants.

It is very similar to an Inconvertible Currency System whereinto the “e-Notes” derive their value from the sheer confidence placed in the issuer. The e-Money System is, in fact, a Fiduciary Money infrastructure and, as such, TRUST is the overarching principle. Let’s elaborate upon this subject a bit before explaining this core FIM‘s Component.

B. THE ECONOMIC FRAMEWORK UNDERPINNING PAYMENTS SYSTEMS

A Payment is a discharge of an obligation by the transfer of Currency Units. Currency is any “Legal Tender” acknowledged as such by statute or law, and embodied in a Monetary Instrument or Medium as to make it “Portable” in “Transfers“. The Payment itself is usually mandated as an “extinguishment of a claim effected by the transfer of Legal Tender, meaning, currency“.

A Means of Payment is any instrument, regardless of the type, technique or procedure used, that facilitates the transfer of funds, between a Debtor and a Creditor.

The Obligation, the claim derived from an Economic Exchange of Goods or its value, becomes “extinct” at the moment a Creditor accepts the “transfer” from the Debtor.

The Transfer of Funds might be carried out in Specie or Book Entries. In a cash transaction, cash is exchanged by means of Bank Notes, coins or bills. In a cashless transaction, the transfer is effected by Debiting the Debtor’s Account and Crediting the Creditor’s Account as happens when the Means of Payment uses a “Bank Money transfer“.

C. THE NATURE OF THE E-MONEY MANAGEMENT SYSTEM

Returning to the issue of Confidence,

How will an e-Money Management System pave the road for a Cashless Economy that will foster Total Financial Inclusion?

To unleash the thread of understanding for such a complex issue, let’s clarify how the “Confidence” is cascaded from the Inconvertible Currency System to a Convertible Currency System, such as the e-Money Management that support the Financial Inclusion Initiative.

First off, the national currency which, in my case is the Dominican Peso, is purely Fiat Money. To propel e-Money to the stature of surrogate “Money”, the e-Money Management system should undertake the endeavor to issue the surrogate currency in such a way that it mirrors the same properties of the Legal Tender. The way we can achieve this mammoth task is by enacting an e-Money System which operates under such rules that will give e-Money the standing of Fiduciary Money. The Fiduciary “role” is to be taken by the Bank which undertakes setting up the Financial Inclusion Model implementation.

With the foregoing background unveiled, let’s tackle the issue of “Money” as proffered by the Financial Inclusion Model. And to make a long matter short, I will just deal here, as promised, with the e-Money Management System component.

C.1 Features of the e-Money Management System

The e-Money Management system comprise an e-Purse, e-Float or e-Currency management platform. The platform usually refers to a specialized computer platform tasked with the following functions:

- Managing the individual accounts (e-Money or Wallet Accounts)

- Managing the interfaces between the Channels or Point of Access whereby the consumers effect the “Payment Orders” which result in Transfers from a Debtor Account to a Creditor Account.

- Managing the Security of the e-Money System (Avoiding fake e-money, reporting data to a System Supervisor, detecting and monitoring the state of the e-money system, etc).

- Running the System Supervisor in charge of monitoring the whole “equilibrium” of the e-Money System.

- Managing the Issuance, Redemption, and Transfer of e-Money.

C.2 Regulatory Issues with regard to e-Money Issuance

Due to the depth and scope of this document I won’t navigate all the threads of compliance and regulation with regards to e-Money. It shall suffice to declare that, in adopting the model, the bank undertakes a Fiduciary Role akin to the State issuing the Legal Tender by which all Economic Obligations are redeemed. By taking on this Fiduciary Role, the Bank becomes a de facto issuer of e-Money, warranting purse holders the full amount of their balance and ascertaining full convertibility into Bank Money or Legal tender upon request from the client.

Banks committing to issuing e-Money are just laying the foundation to become the pillars of trust in the Future Payment Systems Architecture. An ineluctable path shall I say!

The main regulatory issues involved in e-Money Dealing are:

- e-Money must be issued in the same currency as the Legal Tender enacted by law in the host country.

- e-Money could be presented as an alternative to Fiduciary money without pretending to take the role of the legal tender.

- e-Money should be acknowledged as a means of payment with Payment Finality alike that of cash.

- e-Money currency units must be valued the same as the Legal Tender Currency Units.

- There should not be an Exchange rate between e-Money and Legal Tender.

- Banks shall be responsible for the whole lump sum of e-Money Currency in circulation.

- Banks (Issuers) debt must always amounts to the consolidated funds in purse holders individual balance.

- Banks Should be capable of assuring the “Purse Holders Consumers” their funds are equally valuable as Bank Money (i.e. Deposits) as they are in e-Money.

- Banks should be able to assure the e-Money balance is perfectly convertible to Deposits or Cash and vice versa.

- The e-Money System enacts a truly unique Means of Payments with innovative capabilities and benefits for all stakeholders.

C.3 Interfacing the Future and Traditional Payments Instruments

One of the main features brought up by the e-Money Management System is the transparent and smooth co-existence of today’s and future Payments Instruments.

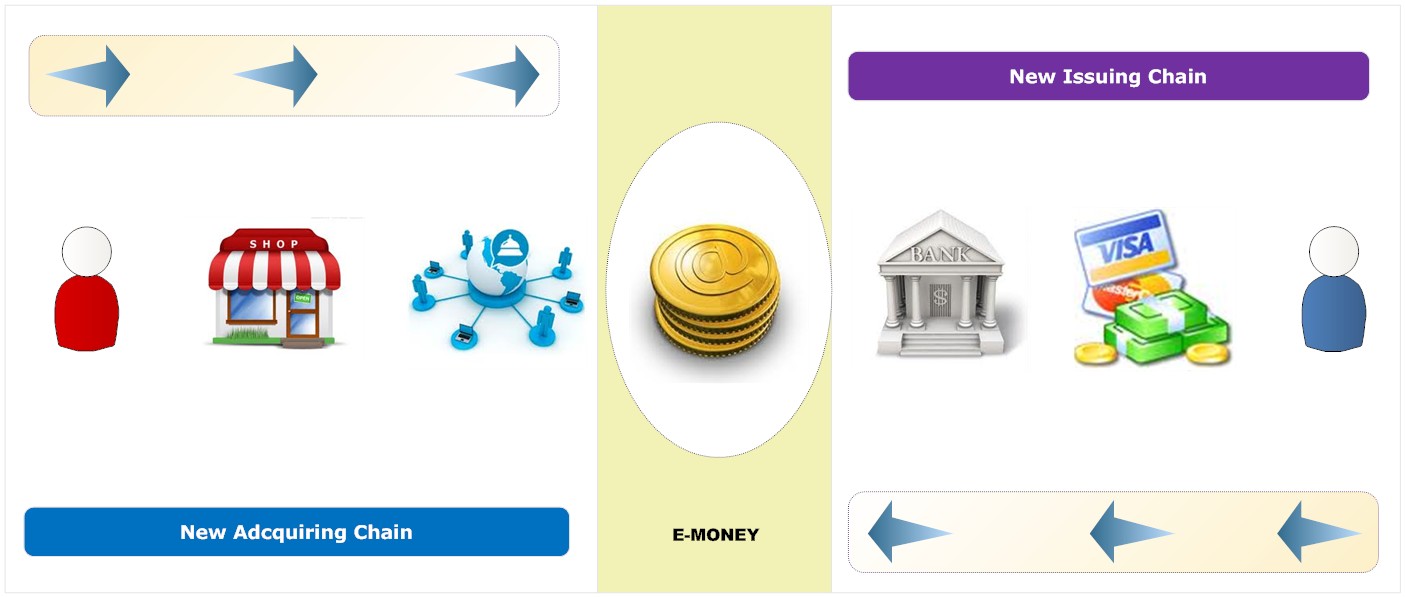

Fig 1. E-Money Value Chain

E-money creates a new Payments Value Chain. Current payments instruments become sources of funds. The new Acquiring Model sprawls a virtually leveled frictionless environment wherein any banking transaction is possible.

In this conjoined, virtually intertwined venue, your past financial user standing becomes irrelevant. It does not matter if you are a traditional bank account holder or a newcomer e-Money (previously unbanked) account bearer; the moment you accept a transfer your account is set up on the spot, and you become fully capable of receiving or issuing any payment order to whatever counterpart is partaking in the e-Money Payments infrastructure. And the e-Money System is construed to interface other siblings implementations, clearly staging direction to a new wave of Clearing and Settlement institutions.

C.4 The Benefits of e-Money

E-Money has a bunch of advantages over Cash. Let’s review those from the stakeholders vantage point:

- For the Merchant receiving payments: Payment is “final” as long as the funds have already being paid. In this regard, e-Money “Payment Finality” is better than that of Credit Cards and Cheques. Only cash rivals this benefit but, we all know the variegated disadvantages of Cash payments.

- e-Money dematerializes Cash: In so doing, Cash Payment transparency issue is solved. Many parties assure that, by dematerializing cash, the economy could reap a range of virtues; among the most notable are: (i) obliterating the preferred criminals’ means of payments;(ii) Making all transfers accessible to regulators and supervisors; (ii) reducing operating costs and fostering innovative Financial Services; (iv) stimulating Financial Inclusion; and last, but not least important, (v) providing an RTGS-like payment systems to a previously underserved population.

- For the Issuer Bank: e-Money represents new markets and fresh funds to foster growth and profitability but, also, from an Economic Vantage Point, e-money issuance becomes self adjustment issue in terms of creating Social and Economic Value. The financial sector has always been perceived as one better serving the rich with little or no focus on the lower ranks of society.

- For the Consumer: Once e-Money is “loaded”, any wallet holder can execute transaction from multiple Points of Contact. And here’s the Icing on the Cake: Once the right components are set in place, you could get a whole country to partake in financial services by just subscribing their phone. Every citizen holding a Mobile Phone could be assigned a Mobile Money Account (i.e. Wallet). Granted, you must solve the convertibility issue first. Thereafter, everybody could be accepting e-Money as a means of payment in no time. Banked and Unbanked population can transparently and smoothly exchange Electronic Value, effectively achieving global Financial Inclusion for a host country.

- For the Host Country: The Host Country benefits from acknowledging the “stealth” economy. Funds transfers become accessible and traceable. Informal Economy, around 60% in DR, surfaces its long-time-buried head and the state income may get a boost to boot. And, just to finish up, the poor’s economics might get a bit better.

Bear with me, when I say that by issuing e-Money and implementing the necessary components, Global Financial Inclusion becomes absolutely possible in shorter terms than presumed by the difficulties arising from current solutions. I will elaborate on this aforementioned thesis in the Bridge-To-Cash and The Bridge-To-Float components.

….Stay tuned!